Like many other asset classes, currency-hedged global bonds sold off in 20221 as spiking global inflation and the aggressive monetary policy tightening response by central banks weighed on broad investment-grade fixed income and equity markets alike.

For some fixed income investors, the magnitude of the drawdowns in fixed income last year might have appeared alarming. Maximum drawdowns in hedged global bonds in 2022 rivalled those seen in other asset classes which are traditionally considered riskier and more volatile than bonds2. But drawdowns in global fixed income markets should not distract investors from the crucial role that bonds can play as a volatility dampener in their portfolios.

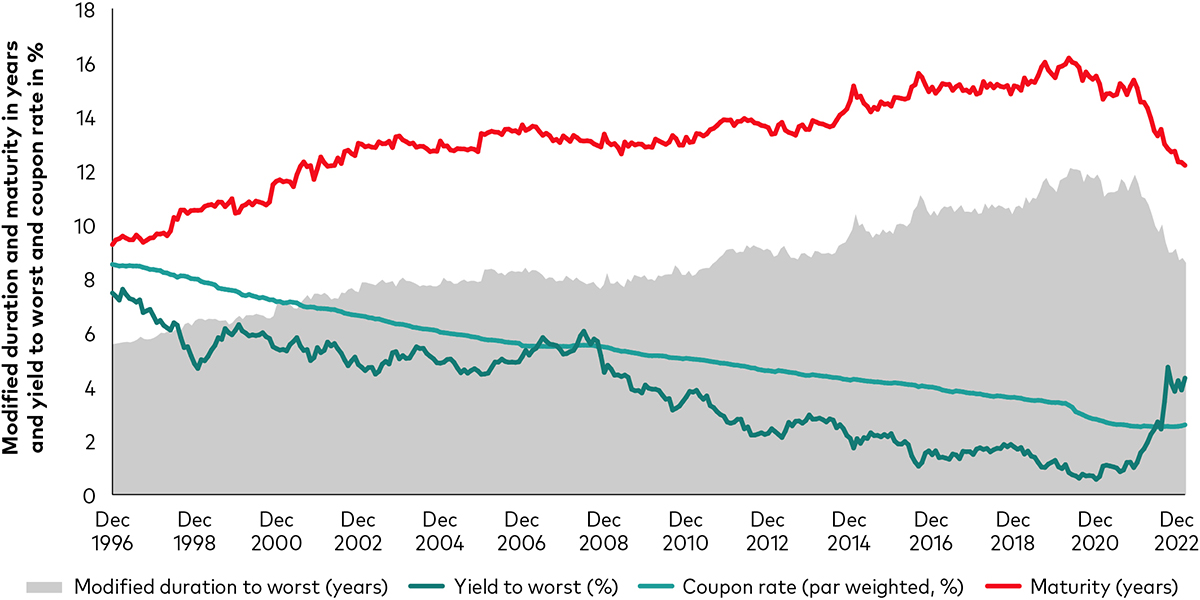

The unravelling of duration risk

As major central banks instigated exceptional monetary stimulus measures in the wake of the global financial crisis, this helped to drive down both short- and long-dated bond yields to historic lows, benefitting returns in investment-grade fixed income markets and riskier asset classes.

Sovereign and corporate debt issuers took advantage by locking in low rates and extending principle repayment through ultra-long bond issues, and investors in turn sought yield increasingly further out on the risk and maturity spectra. As a result, duration risk—the sensitivity of a bond's price to changes in interest rates accounting for characteristics of the bond such as yield, coupon rate and maturity—steadily built up, as the chart shows.

Duration risk steadily built up - then rapidly unravelled

Source: Bloomberg, Vanguard. Broad GBP bond market represented by the Bloomberg Sterling Aggregate Index. Data from 31 December 1996 to 28 February 2023.

Then, in 2022, this duration risk unravelled as global monetary conditions abruptly reversed and central banks ended bond purchasing programmes and raised policy rates. This caused yields across fixed income sub-asset classes to rise. For investors, this led to magnified losses in bond markets on a scale normally associated with equities, with double-digit maximum drawdown percentages for most investment-grade fixed income categories—global bonds inclusive—as well as in most other major asset classes.

One important point to bear in mind here is that, with duration risk now significantly lower (and policy rates substantially higher) than investors have experienced for several years, the risk of similarly large drawdowns in global bonds is reduced3.

But fixating on bond drawdowns in isolation also risks diverting investors' attention from one of the core reasons why many of them invest in fixed income in the first place. In reality, investors typically own bonds alongside other asset classes in portfolios, and most of them therefore prize the shock-absorbing qualities of fixed income - rather than holding bonds purely as a performance proposition.

Viewed through this lens, we believe that volatility—as measured by annualised standard deviation—is a more relevant measure of the recurrent risks facing long-term investors in global bonds than maximum drawdown, which is more associated with tail risk, or the risk of low-probability events.

Using volatility as a yardstick, hedged global bonds were one of the best tools in helping investors weather the turbulent markets of 2022 and act as a shock absorber relative to other asset classes in multi-asset portfolios. The table below shows the volatility and maximum drawdown of a range of asset classes in 2022.

2022 was a year of risks for many asset classes

|

Asset class |

Volatility |

Maximum drawdown |

|

Commodities |

24.75% |

-16.66% |

|

Global all-cap equities |

14.69% |

-15.25% |

|

Global aggregate bonds (unhedged) |

8.20% |

-7.26% |

|

Global aggregate bonds (hedged) |

5.81% |

-14.31% |

Source: Bloomberg, Vanguard. Data from 31 December 2021 to 30 December 2022. Volatility represented by standard deviation, annualised. Annualisation is based on weekly total returns. Benchmarks used as proxies: Commodities - Bloomberg Commodity Index Total Return; global all-cap equities - MSCI ACWI IMI Net Total Return Index; global aggregate fixed income - Bloomberg Global-Aggregate Total Return Index; global aggregate fixed income hedged to GBP - Bloomberg Global-Aggregate Total Return Index Hedged GBP.

When assessed according to volatility, there are few viable alternatives to hedged global bonds as a diversified portfolio building block to reduce portfolio risk, in our view.

In addition to providing investors cost-effective access to a diversified universe of nearly 30,000 underlying bonds4, global hedged bonds had one of the lowest levels of volatility among major asset classes in 2022 during what was generally a volatile year for financial markets.

In 2022, hedged global bonds had a volatility of 5.81%, which compares favourably to the volatility profile of global all-cap equity markets (14.69%), which many investors are looking to hedge with global bonds. Elsewhere, broad commodity exposures5 had a volatility of 24.75%.

One reason that global bonds were able to offer investors relatively low volatility in an otherwise turbulent market environment was down to the global diversification between local bond markets as individual central banks responded differently to inflation and growth expectations in their respective markets as 2022 unfolded.

The importance of hedging global bonds

Overlaying a currency hedge to foreign-currency bonds also helped to dampen the volatility of global bond portfolios - an important feature given the relative high volatility of currencies, especially those which are highly correlated with the bond market in that country.

Compared with unhedged global bonds, hedged global bonds' volatility of 5.81% was lower than the 8.20% volatility of the unhedged equivalent, underscoring the shock-absorbing effect of hedging bond exposures to an investor's local currency.

Exchange-rate volatility can amplify the volatility of overseas bond exposures when translated into an investor's home currency. For example, if a particular foreign currency depreciates relative to an investor's home currency at the same time that bond prices in that foreign market fall, the decline translated into the investor's home currency will be larger. Currency hedging overseas bond exposures back into the domestic currency can help bond investors to reduce volatility while maintaining returns.

After a tough 2022, we expect that fixed income investors are set for a brighter 2023. And over the long term—thanks to their risk-dampening properties—hedged global bonds will remain an integral and enduring building block in multi-asset portfolios.

This post is funded by Vanguard

1 Source: Bloomberg, 31 December 2021 to 30 December 2022. Global aggregate fixed income hedged to GBP, as represented by the Bloomberg Global-Aggregate Total Return Index Hedged GBP, returned -12.15% from 31 December 2021 to 30 December 2022.

2 Source: Bloomberg, 31 December 2021 to 30 December 2022. From 31 December 2021 to 30 December 2022, the maximum drawdowns in Global aggregate fixed income hedged to GBP (as represented by the Bloomberg Global-Aggregate Total Return Index Hedged GBP), commodities (as represented by the Bloomberg Commodity Index Total Return) and global all-cap equities (as represented by the MSCI ACWI IMI Net Total Return Index) were -14.31%, -16.66% and -15.25% respectively.

3 Source: Vanguard.

4 Source: Bloomberg as at 20 March 2023. The Bloomberg Global Aggregate Float Adjusted and Scaled Index in GBP had 29,211 constituents as at 28 February 2023.

5 Source: Bloomberg, 31 December 2021 to 30 December 2022. Benchmarks used as proxies: Commodities - Bloomberg Commodity Index Total Return; global all-cap equities - MSCI ACWI IMI Net Total Return Index; global aggregate fixed income hedged to GBP - Bloomberg Global-Aggregate Total Return Index Hedged GBP.

Investment risk information

The value of investments, and the income from them, may fall or rise and investors may get back less than they invested.

Past performance is not a reliable indicator of future results.

Funds investing in fixed interest securities carry the risk of default on repayment and erosion of the capital value of your investment and the level of income may fluctuate. Movements in interest rates are likely to affect the capital value of fixed interest securities. Corporate bonds may provide higher yields but as such may carry greater credit risk increasing the risk of default on repayment and erosion of the capital value of your investment. The level of income may fluctuate and movements in interest rates are likely to affect the capital value of bonds.

Important information

For professional investors only (as defined under the MiFID II Directive) investing for their own account (including management companies (fund of funds) and professional clients investing on behalf of their discretionary clients). In Switzerland for professional investors only. Not to be distributed to the public.

The information contained in this document is not to be regarded as an offer to buy or sell or the solicitation of any offer to buy or sell securities in any jurisdiction where such an offer or solicitation is against the law, or to anyone to whom it is unlawful to make such an offer or solicitation, or if the person making the offer or solicitation is not qualified to do so. The information in this document does not constitute legal, tax, or investment advice. You must not, therefore, rely on the content of this document when making any investment decisions.

The information contained in this document is for educational purposes only and is not a recommendation or solicitation to buy or sell investments.

Issued in EEA by Vanguard Group (Ireland) Limited which is regulated in Ireland by the Central Bank of Ireland.

Issued in Switzerland by Vanguard Investments Switzerland GmbH.

Issued by Vanguard Asset Management, Limited which is authorised and regulated in the UK by the Financial Conduct Authority.

© 2023 Vanguard Group (Ireland) Limited. All rights reserved.

© 2023 Vanguard Investments Switzerland GmbH. All rights reserved.

© 2023 Vanguard Asset Management, Limited. All rights reserved.