Despite a volatile market environment, interest in sustainable investing strategies has never been stronger, as more investors seek to align their sustainability beliefs with their investing choices.

Assets held in environmental, social and governance (ESG) funds have almost doubled since 2018 to nearly $3 trillion1, with Europe accounting for 84% of the total market. Sustainable funds now account for more than 20% of the total European fund universe2.

ESG index funds: a popular choice

Much like standard indexing strategies, ESG index funds and ETFs aim to mirror the performance and composition of a financial market index. In this case, they are replicating ESG indices that screen the constituents of a standard benchmark index based on certain ESG criteria, as determined by the index provider.

- Exclusionary: Avoids or reduces exposure to certain activities that many investors view as controversial, such as firearms, tobacco or fossil fuels.

- Inclusionary: Includes companies that meet certain ESG standards, or adjust the company weightings, based on their ESG ratings, data or the asset manager's proprietary assessment.

- Thematic: Focuses on companies that contribute to specific ESG themes or goals, such as clean technology or water management.

ESG indices are, by implication, less diversified than their parent benchmarks - although the level of diversification can vary widely from fund to fund3. Exclusionary indices, for example, typically retain up to 80% of the securities in a broad equity market index4, while a ‘best-in-class' approach can capture less than 50% of the constituents in its parent benchmark5,6.

At Vanguard, we consider our ESG index funds and ETFs to carry active risk because their holdings deviate from those of standard benchmark indices. This can impact the risk and return characteristics of ESG indices relative to their (non-ESG) parent benchmarks - and can therefore impact the risk profile of portfolios using ESG index building blocks in place of traditional (non-ESG) index funds and ETFs.

Consequently, when advisers are constructing portfolios with ESG building blocks, they need to take into account the unique risk-return characteristics of the ESG components in their asset allocation to ensure the portfolio maintains its optimised balance of risk and return.

Will adding ESG index funds change the level of risk in a portfolio?

For many advisers, the greatest challenge to incorporating ESG building blocks into client portfolios is understanding the potential impact on performance. When a client expresses an ESG preference, how are their needs best met while ensuring the portfolio is still meeting its broader risk and return goals?

Due to the differences in the risk profiles of ESG building blocks, we know that incorporating them into a portfolio isn't as simple as swapping out traditional (non-ESG) index building blocks with their ESG alternative. Doing so could run the risk of the ESG portfolio having a suboptimal asset allocation, and returns that are higher or lower than traditional portfolio-based expectations.

To address these potential portfolio biases, they need to be considered during the portfolio construction process. Modelling tools such as Vanguard's proprietary active-passive framework, the Vanguard Asset Allocation Model® (VAAM®) and long-term capital market forecasts generated by the Vanguard Capital Markets Model (VCMM) can help us optimise asset allocations by adjusting the weightings to reflect the unique risk-return characteristics of the underlying ESG (and non-ESG) building blocks.

This approach to portfolio construction could be applied to all types of ESG investments, including inclusionary and thematic as well as exclusionary - offering a flexible modelling solution for constructing efficient portfolios that meet the investment goals and ESG preferences of individual clients.

A hypothetical example

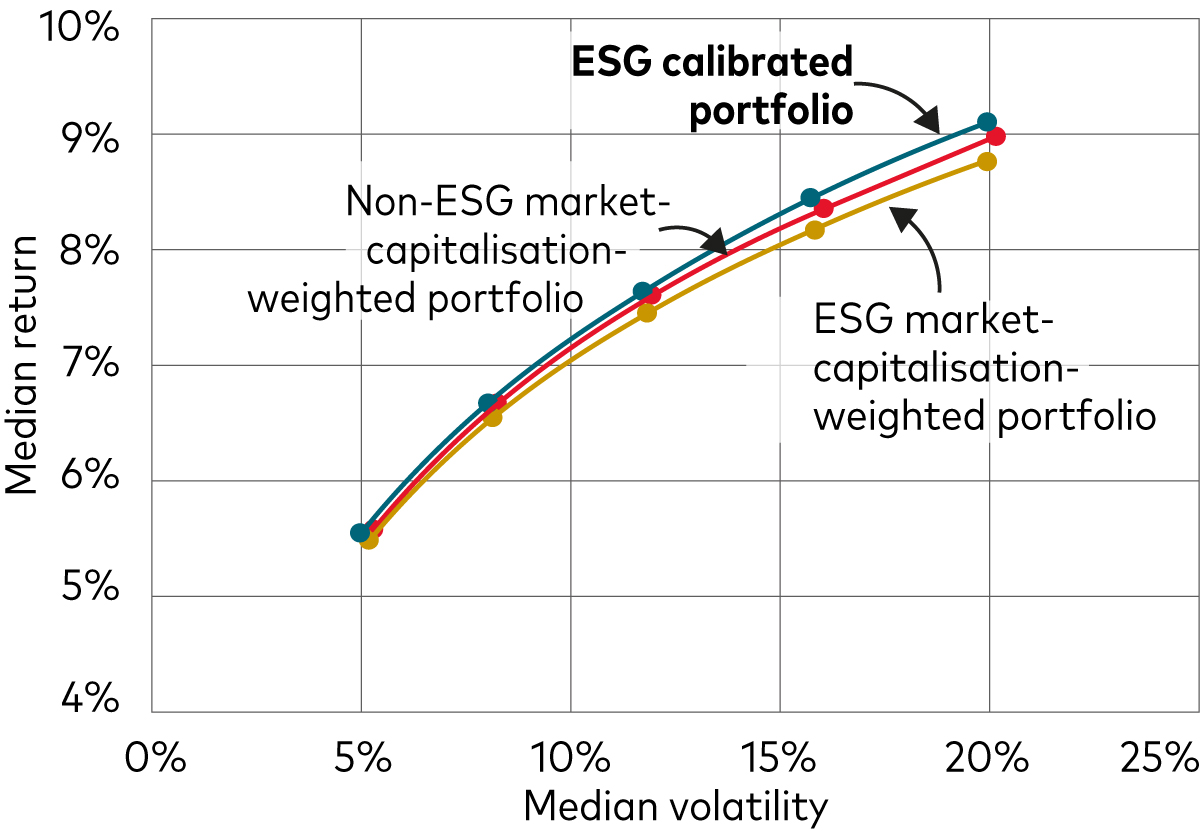

The graph below helps illustrate the potential benefits of Vanguard's approach to incorporating ESG criteria into portfolios. Here, we see the forecasted efficient frontiers7 for three hypothetical portfolio scenarios:

- the red line represents a traditional portfolio constructed with non-ESG index funds weighted at historical sample market-cap averages;

- the yellow line represents an ESG portfolio constructed with ESG index funds also weighted at historical sample market cap averages; and

- the blue line represents a portfolio constructed with ESG index funds weighted at their steady-state optimised allocations8 derived from the VAAM and VCMM.

10-year annualised average expected risk and returns for a hypothetical ESG-calibrated portfolio9

Any projections should be regarded as hypothetical in nature and do not reflect or guarantee future results.

Source: Vanguard. Projections based on a 10-year time horizon and are as at 30 June 2022. Calculations are on a projected nominal return basis, in EUR. See footnote (9) for additional details.

As the graph shows, replacing traditional index building blocks in a market-cap-weighted portfolio (red line) with ESG building blocks results in a sub-optimal risk-return profile (yellow line). Yet when we calibrate the asset allocation based on the risk factors of the ESG building blocks, the result is an optimised portfolio frontier (blue line) that meets or exceeds the forecasted annualised returns of the traditional market cap-weighted portfolio (red line).

A long-term solution

There are many reasons why investors may choose to include ESG funds in their investment choices. We show how advisers can incorporate ESG strategies while still meeting their clients' long-term investment objectives.

Vanguard's approach to ESG investing

With more than 50 million clients globally who look to us to both safeguard and grow their investments, we think about environmental, social and governance (ESG) issues in the context of delivering long-term value to our investors and helping them to meet their objectives.

Notes

1 Source: Morningstar Global Sustainable Fund Flows: Q2 2023 in Review, 26 July 2023.

Total global sustainable assets were worth $1.4 trillion at the end of 2018 and $2.8 trillion as at 31 March 2023. Morningstar defines the ‘global sustainable fund universe' as open-end funds and ETFs that, by prospectus or other regulatory filings, claim to focus on sustainability; impact; or environmental, social, and governance factors. They exclude ‘ESG integrated funds'; funds that employ limited exclusionary screens such as controversial weapons, tobacco, and thermal coal; and money market funds, feeder funds, and funds of funds to avoid double counting assets.

2 Source: Morningstar. Sustainable fund assets accounted for 22% of the European fund universe, as at 31 March 2023.

3 ESG index providers have their own discretionary sets of screening rules, which can result in significant differences in the underlying security constituents of ESG indices. At Vanguard, we use ESG index providers that apply a revenue-based screening methodology which groups companies involved in certain business activities according to three levels of restrictiveness. Within each level, the indices exclude companies that exceed certain revenue thresholds. The thresholds vary based on whether the involvement is primary or secondary to their business. Within our most restrictive category, for instance, the threshold is 0% for both primary and secondary involvement.

4 Source: Vanguard. Based on an analysis of FTSE All Choice index funds and ETFs, as at June 2023.

5 ‘Best-in-class' strategies combine an exclusionary screening to avoid exposure to certain companies and industries in their parent benchmark, with an inclusionary screening of the remaining companies to select only those with best practices, typically using the companies' ESG ratings as metrics for the inclusionary screening.

6 Source: Vanguard. Based on an analysis of ESG index funds and ETFs that screen the MSCI ACWI, as at June 2023.

7 An ‘efficient frontier' represents the highest expected return with the lowest possible risk across the risk spectrum for a portfolio of assets.

8 ‘Steady state optimised allocation' refers to a portfolio with fixed levels of exposure to its underlying building blocks within each asset class.

9 The efficient frontiers are built using VCMM simulations for the following asset classes: North America equity, Developed Europe equity, Developed Asia Pacific equity, Emerging Markets equity, Global Corporate bonds, EUR government bonds and US government bonds. The Non-ESG market cap-weighted portfolio's efficient frontier represents the 10-year forecasted annualised median return and median annualised volatility for a multi-asset portfolio constructed with traditional, non-ESG indices weighted at their historical sample market cap average. The ESG market cap-weighted portfolio's efficient frontier represents the 10-year forecasted annualised median return and median annualised volatility for a multi-asset portfolio constructed with ESG indices weighted at their historical sample market cap average. The ESG calibrated portfolio's efficient frontier represents the 10-year forecasted annualised median return and median annualised volatility for a multi-asset portfolio constructed with ESG indices weighted at their steady-state optimised allocation derived from the VAAM®.

Investment risk information

The value of investments, and the income from them, may fall or rise and investors may get back less than they invested.

Past performance is not a reliable indicator of future results.

Any projections should be regarded as hypothetical in nature and do not reflect or guarantee future results.

ETF shares can be bought or sold only through a broker. Investing in ETFs entails stockbroker commission and a bid- offer spread which should be considered fully before investing.

IMPORTANT: The projections and other information generated by the Vanguard Capital Markets Model regarding the likelihood of various investment outcomes are hypothetical in nature, do not reflect actual investment results and are not guarantees of future results. VCMM results will vary with each use and over time.

The VCMM projections are based on a statistical analysis of historical data. Future returns may behave differently from the historical patterns captured in the VCMM. More important, the VCMM may be underestimating extreme negative scenarios unobserved in the historical period on which the model estimation is based.

The Vanguard Capital Markets Model® is a proprietary financial simulation tool developed and maintained by Vanguard's primary investment research and advice teams. The model forecasts distributions of future returns for a wide array of broad asset classes. Those asset classes include US and international equity markets, several maturities of the U.S. Treasury and corporate fixed income markets, international fixed income markets, U.S. money markets, commodities, and certain alternative investment strategies. The theoretical and empirical foundation for the Vanguard Capital Markets Model is that the returns of various asset classes reflect the compensation investors require for bearing different types of systematic risk (beta). At the core of the model are estimates of the dynamic statistical relationship between risk factors and asset returns, obtained from statistical analysis based on available monthly financial and economic data from as early as 1960. Using a system of estimated equations, the model then applies a Monte Carlo simulation method to project the estimated interrelationships among risk factors and asset classes as well as uncertainty and randomness over time. The model generates a large set of simulated outcomes for each asset class over several time horizons. Forecasts are obtained by computing measures of central tendency in these simulations. Results produced by the tool will vary with each use and over time.

Important information

For professional investors only (as defined under the MiFID II Directive) investing for their own account (including management companies (fund of funds) and professional clients investing on behalf of their discretionary clients). In Switzerland for professional investors only. Not to be distributed to the public.

The information contained in this document is not to be regarded as an offer to buy or sell or the solicitation of any offer to buy or sell securities in any jurisdiction where such an offer or solicitation is against the law, or to anyone to whom it is unlawful to make such an offer or solicitation, or if the person making the offer or solicitation is not qualified to do so. The information in this document does not constitute legal, tax, or investment advice. You must not, therefore, rely on the content of this document when making any investment decisions.

The information contained in this document is for educational purposes only and is not a recommendation or solicitation to buy or sell investments.

Issued in EEA by Vanguard Group (Ireland) Limited which is regulated in Ireland by the Central Bank of Ireland.

Issued in Switzerland by Vanguard Investments Switzerland GmbH.

Issued by Vanguard Asset Management, Limited which is authorised and regulated in the UK by the Financial Conduct Authority.

© 2023 Vanguard Group (Ireland) Limited. All rights reserved.

© 2023 Vanguard Investments Switzerland GmbH. All rights reserved.

© 2023 Vanguard Asset Management, Limited. All rights reserved.